BIC贝叶斯信息准则(用于解决ARIMA模型中q、p参数选择问题)

贝叶斯信息准则,也称为Bayesian Information Criterion(BIC)

1.定义和公式

其中k为模型参数的个数,n为样本的数量,L为似然函数。

模型评估标准:BIC值越低越好。

p和q越大时,参数越多,k越大。所以使k越小,p和q越小,保证模型越好。

L越大,使BIC的值越小,所以似然函数越大越好。

二、代码实现

开发环境:Jupyter Anaconda3

首先需要训练一个ARIMA模型来进行估计,这里我选择使用2015年至2020年道琼斯的时间序列数据集。

1、先导入所需第三方库及依赖

%load_ext autoreload

%autoreload 2

%matplotlib inline

%config InlineBackend.figure_format='retina'

from __future__ import absolute_import, division, print_function

import sys

import os

import pandas as pd

import numpy as np

# TSA from Statsmodels

import statsmodels.api as sm

import statsmodels.formula.api as smf

import statsmodels.tsa.api as smt

# Display and Plotting

import matplotlib.pylab as plt

import seaborn as sns

pd.set_option('display.float_format', lambda x: '%.5f' % x) # pandas

np.set_printoptions(precision=5, suppress=True) # numpy

pd.set_option('display.max_columns', 100)

pd.set_option('display.max_rows', 100)

# seaborn plotting style

sns.set(style='ticks', context='poster')

2、导入数据并做一下数据预处理

filename_ts = 'data.csv'

ts_df = pd.read_csv(filename_ts, index_col=0, parse_dates=[0])

n_sample = ts_df.shape[0]

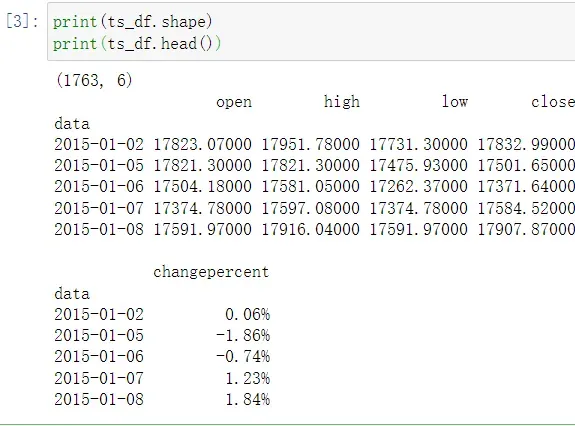

print(ts_df.shape)

print(ts_df.head())

处理后的时间序列数据集如下所示:

3、设置置信区间和需要训练的列

这里我选择闭盘的数据close列

n_train=int(0.95*n_sample)+1

n_forecast=n_sample-n_train

#ts_df

ts_train = ts_df.iloc[:n_train]['close']

ts_test = ts_df.iloc[n_train:]['close']

print(ts_train.shape)

print(ts_test.shape)

print("Training Series:", "\n", ts_train.tail(), "\n")

print("Testing Series:", "\n", ts_test.head())

4、模型评估

获得训练数据集后,您可以执行模型评估

#模型评估

# Fit the model

arima200 = sm.tsa.SARIMAX(ts_train, order=(1,0,0))#order里边的三个参数p,d,q

model_results = arima200.fit()#fit模型

BIC

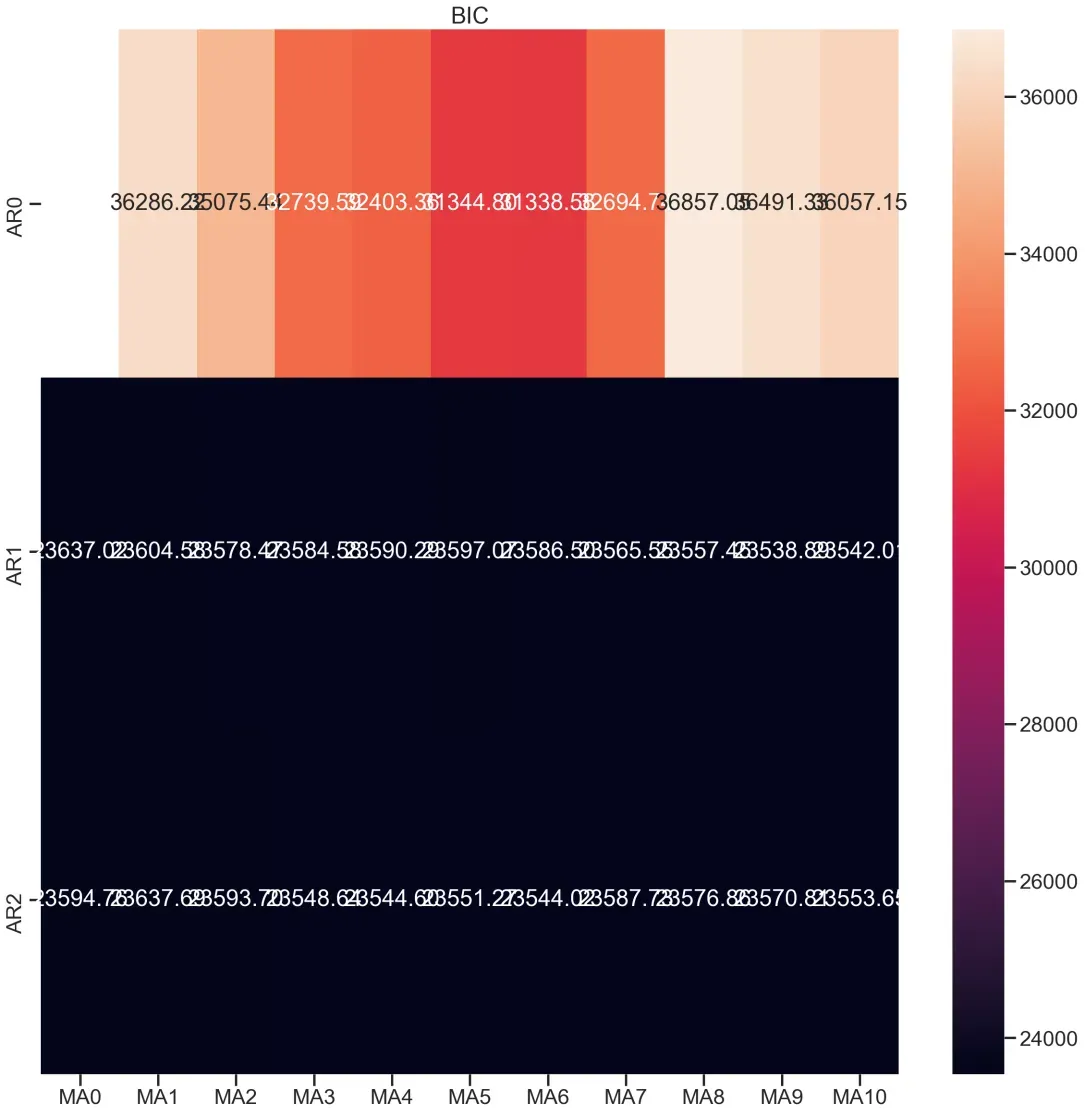

这里我之前通过绘制ACF和PACF的图像对p、q值的取值范围有了一定的了解,所以p、q值的最大范围做了最小限定。

import itertools

#当多组值都不符合时,遍历多组值,得出最好的值

p_min = 0

d_min = 0

q_min = 0

p_max = 2

d_max = 0

q_max = 10

# Initialize a DataFrame to store the results

results_bic = pd.DataFrame(index=['AR{}'.format(i) for i in range(p_min,p_max+1)],

columns=['MA{}'.format(i) for i in range(q_min,q_max+1)])

for p,d,q in itertools.product(range(p_min,p_max+1),

range(d_min,d_max+1),

range(q_min,q_max+1)):

if p==0 and d==0 and q==0:

results_bic.loc['AR{}'.format(p), 'MA{}'.format(q)] = np.nan

continue

try:

model = sm.tsa.SARIMAX(ts_train, order=(p, d, q),

#enforce_stationarity=False,

#enforce_invertibility=False,

)

results = model.fit()

results_bic.loc['AR{}'.format(p), 'MA{}'.format(q)] = results.bic

except:

continue

results_bic = results_bic[results_bic.columns].astype(float)

可以看一下BIC的输出范围,值越小(黑色区域)越符合,

fig, ax = plt.subplots(figsize=(20, 20))

ax = sns.heatmap(results_bic,

mask=results_bic.isnull(),

ax=ax,

annot=True,

fmt='.2f',

);

ax.set_title('BIC');

这里可以看出我的BIC值范围,其中纵轴AR为自回归模型输出(q的范围),MA为移动平均模型输出(p的范围)

最后输出BIC所判定的p和q的值为1和9。另外还输出了AIC所判定的结果进行对比(在这里不介绍AIC了)。最后我还是通过观察PACF和ACF来进行最终抉择选择BIC输出的q、p值作为参数。

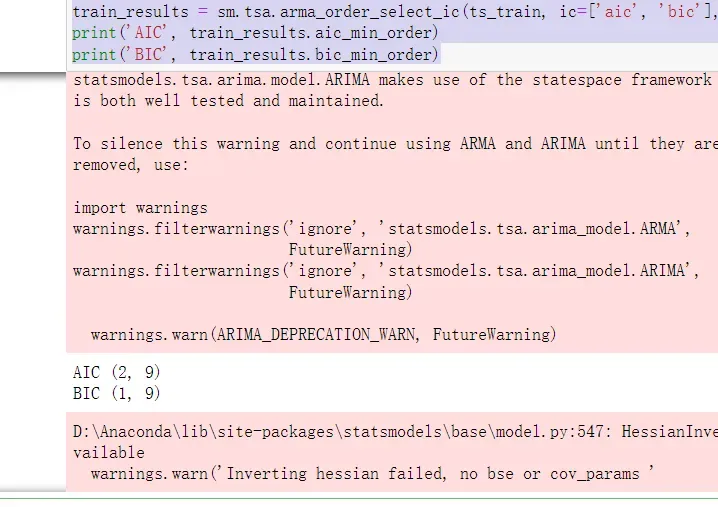

train_results = sm.tsa.arma_order_select_ic(ts_train, ic=['aic', 'bic'], trend='nc', max_ar=2, max_ma=10)

print('AIC', train_results.aic_min_order)

print('BIC', train_results.bic_min_order)

参考https://www.cnblogs.com/tianqizhi/p/9277376.html

文章出处登录后可见!

已经登录?立即刷新